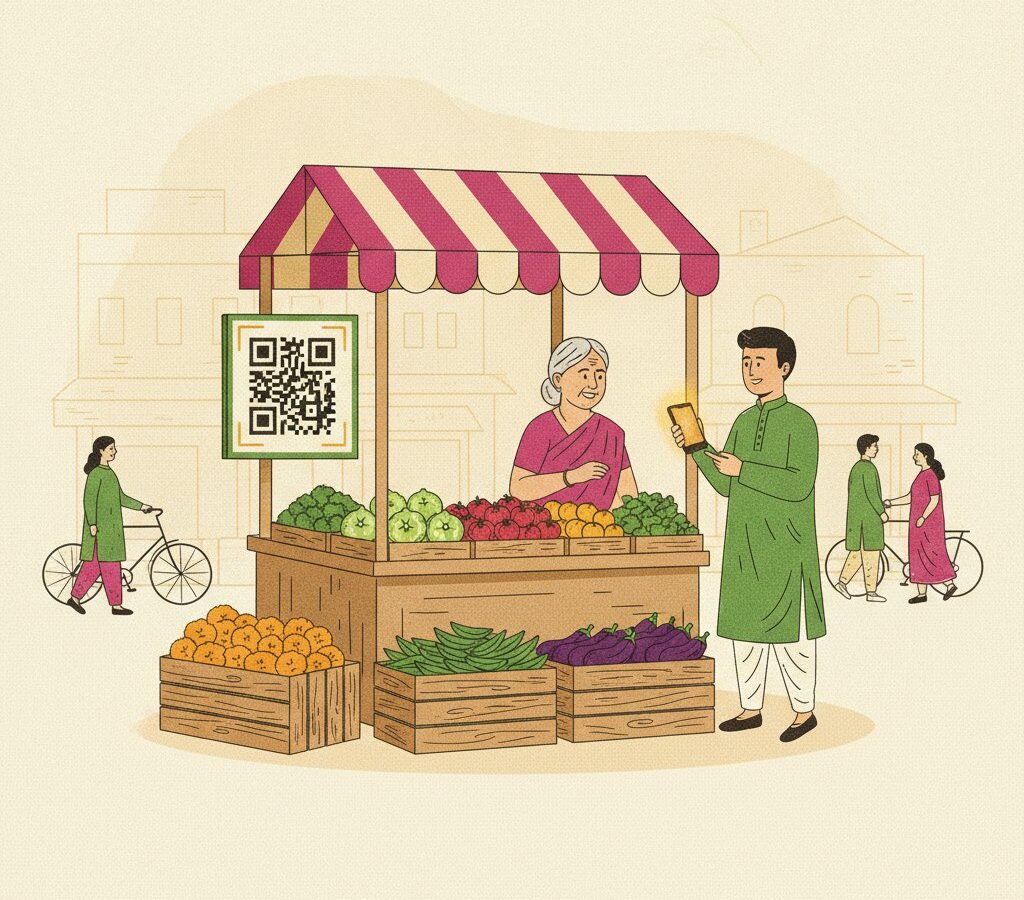

On any given afternoon in an Indian city, a vegetable seller adjusts a hand-painted QR code propped against a pile of tomatoes. A customer scans it, types in twenty rupees, and the transaction is done before the change would have been counted. Neither party needed a credit history, a bank-issued card, or a point-of-sale terminal. That quiet, ordinary moment is the end result of a deliberate piece of public infrastructure built over the past decade.

What UPI Actually Is — and What It Is Not

The Unified Payments Interface was developed by the National Payments Corporation of India, a not-for-profit entity set up under the Reserve Bank of India. NPCI launched UPI in 2016 as a protocol, not a product. The distinction matters: UPI is the underlying rail on which private applications can build. No single company owns it. Every participating bank connects to the same interoperable system, meaning a user on one app can pay someone on a completely different app without friction. Competition happened at the application layer rather than at the payments layer. India’s real-time payments volumes have, by most international comparisons, consistently ranked among the highest in the world — surpassing countries with far larger economies in sheer transaction count.

Who It Reached — and How

The spread was enabled by several converging conditions: the expansion of cheap mobile data, the growth of low-cost smartphones, the pre-existing Jan Dhan bank-account programme that brought hundreds of millions of unbanked Indians into the formal banking system, and a biometric identity infrastructure that simplified verification. Each layer built on the others. Small merchants were among the most visible adopters: the QR code required no hardware, no monthly fee, no card machine. Acceptance by street vendors, auto-rickshaw drivers, and market stalls happened organically, and instant settlement mattered enormously to micro-businesses operating on daily cash cycles.

Why Other Countries Are Studying the Model

Several countries have initiated dialogues with NPCI about adapting the UPI framework. The appeal is the architecture: a publicly governed interoperable layer that prevents any single private actor from controlling the payments chokepoint, combined with a regime that allows private innovation on top. Singapore and India have already piloted a linkage between their respective real-time payment systems, and the World Bank and the Bank for International Settlements have both analysed India’s digital public infrastructure as a potential template for financial inclusion.

The Caveats Worth Keeping in Mind

Honest accounting requires noting what has not been fully resolved. Digital literacy remains uneven, and a portion of rural and elderly populations continue to rely on intermediaries to transact on their behalf rather than operating independently. Privacy architecture has drawn scrutiny, since transaction data flows through a system that does not offer the anonymity of cash. Fraud through social engineering — tricking users into authorising payments — has grown alongside adoption. None of this diminishes the achievement. UPI represents a rare case of public infrastructure that worked at scale, included people previously excluded from formal finance, and created competitive conditions for private innovation without surrendering the commons to private capture.